CHICAGO – August 5, 2019 – Ryerson Holding Corporation (NYSE: RYI), a leading value-added processor and distributor of industrial metals, today reported results for the second quarter ended June 30, 2019.

Q2 2019 Key Metrics:

Management Commentary

Eddie Lehner, Ryerson’s President and Chief Executive Officer, said, “I want to thank our customers for the opportunity to earn your business, which we never take for granted, and my Ryerson colleagues for strong execution in a challenging quarter. Ryerson exceeded our second quarter 2019 revenue guidance with higher tons shipped offset by average selling price declines that were in line with expectations. However, margins declined more than our guidance due to cost of goods sold declining at a slower than expected pace relative to inventory replacement cost. Ryerson’s same-store business units executed well; however, we fell short of the guidance articulated during our first quarter of 2019 earnings call due to Central Steel & Wire (“CS&W”) inventory holding losses of $8 million on long physical customer program account positions, and mark-to-market hedging losses incurred during the quarter of approximately $10 million. Both of these occurrences were primarily a function of the steep drop in hot-rolled coil prices; however, we also experienced the lagging effects of higher cost inbound inventory as spot transaction prices began declining at an accelerating rate. With respect to the mark-to-market hedging losses in the quarter, we expect to regain a significant portion of this “prepaid” margin compression during the second half of 2019 as these hedges expire against the related shipments to our customers.

Eddie continued, “Even though the clock ran out in the second quarter as industry price conditions were bottoming, Ryerson meaningfully increased our book value of equity, generated significant cash from operating activities, and reduced our outstanding debt in the second quarter of 2019. We expect higher gross margin, excluding LIFO in the third quarter of 2019 given the positive inflection in hot-rolled coil and LME Nickel prices, along with a decline in average inventory costs during the period.”

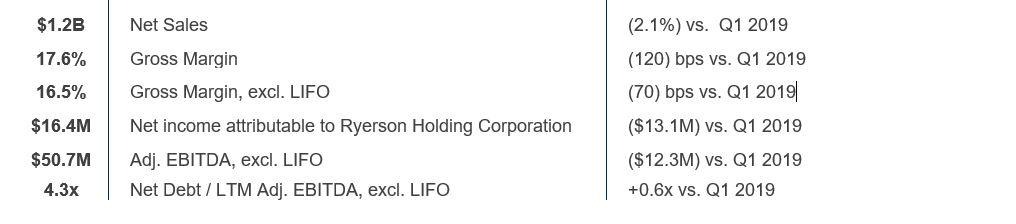

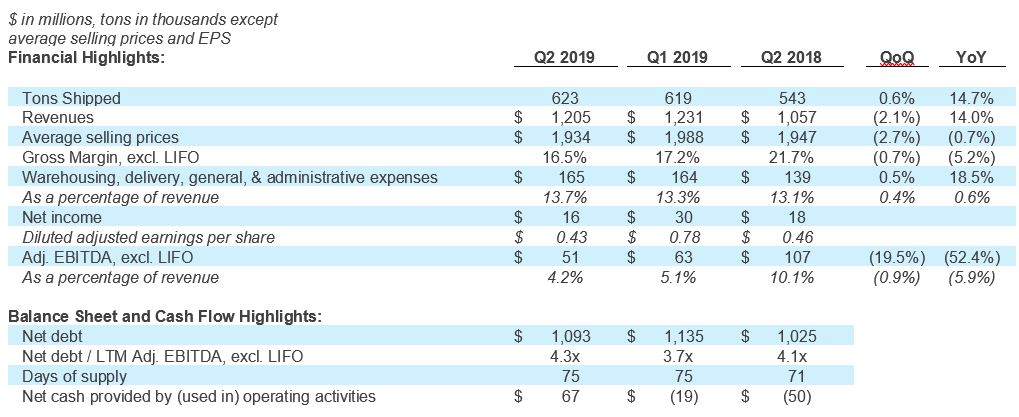

Ryerson achieved revenues of $1.20 billion, an increase of 14.0 percent compared to $1.06 billion in the second quarter of 2018, with tons shipped 14.7 percent higher and average selling prices down 0.7 percent. Excluding the results of our third quarter 2018 acquisition of CS&W, revenues for the quarter were $1.05 billion, flat compared to the same quarter last year with average selling prices 1.6 percent higher and tons shipped down 2.2 percent. Ryerson continued to gain market share during the second quarter of 2019 compared to the second quarter of 2018, as North American industry volume contracted 7.7 percent according to the Metal Service Center Institute, or MSCI, while Ryerson North American same-store tons shipped contracted by only 1.7 percent.

Gross margin was 17.6 percent for the second quarter of 2019, compared to 18.8 percent in the first quarter of 2019, and 17.5 percent for the same quarter last year. Included in cost of materials sold during the second quarter of 2019 was LIFO income of $12.9 million, compared to LIFO income of $20.1 million in the first quarter of 2019, and LIFO expense of $43.9 million in the second quarter of 2018. Gross margin, excluding LIFO was 16.5 percent in the second quarter of 2019 compared to 17.2 percent in the first quarter of 2019, and 21.7 percent in the second quarter of 2018. Margin compression during the second quarter was partially driven by mark-to-market hedging losses and inventory costs falling at a slower rate than average selling prices, most notably at CS&W which continues to work down its large inventory positions in carbon sheet products. A reconciliation of gross margin, excluding LIFO to gross margin is included below in this news release.

Warehousing, delivery, selling, general, and administrative expense increased by $25.7 million, or 18.5 percent in the second quarter of 2019, compared to the year-ago period primarily driven by the acquisition of CS&W. On a same-store basis, expenses decreased by $5.2 million, or 3.7 percent, compared to the second quarter of 2018. Warehousing, delivery, selling, general, and administrative expenses as a percentage of sales increased to 13.7 percent in the second quarter of 2019 compared to 13.1 percent in the second quarter of 2018. However, on a same-store basis warehousing, delivery, selling, general, and administrative expenses as a percentage of sales declined by 40 basis points year-over-year to 12.7 percent, demonstrating Ryerson’s ability to effectively manage costs in any environment across an increasingly responsive variable cost structure.

Net income attributable to Ryerson Holding Corporation was $16.4 million, or $0.43 per diluted share, in the second quarter of 2019 compared to $17.5 million, or $0.46 per diluted share, in the prior year period. Ryerson achieved Adjusted EBITDA, excluding LIFO of $50.7 million in the second quarter of 2019, a decrease of $12.3 million compared to the first quarter of 2019 or $55.9 million less than the second quarter of 2018. A reconciliation of Adjusted EBITDA, excluding LIFO to net income attributable to Ryerson Holding Corporation is included below in this news release.

Six Months Ended June 30, 2019, Financial Results

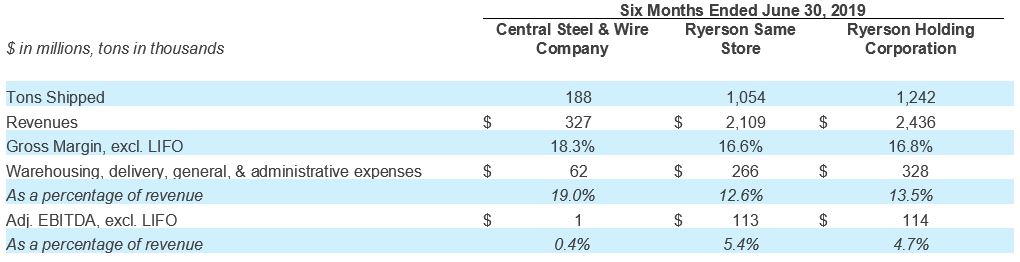

Revenues in the first six months of 2019 were $2.44 billion, an increase of 21.9 percent compared to the first six months of 2018, as tons shipped increased 16.2 percent and average selling prices increased 4.9 percent. On a same-store basis, revenues were $2.11 billion in the first six months of 2019, with average selling prices up 7.1 percent partially offset by a decrease in tons shipped of 1.4 percent.

Net income attributable to Ryerson Holding Corporation was $45.9 million, or $1.21 per diluted share, in the first six months of 2019 compared to $27.9 million, or $0.74 per diluted share, for the same period of 2018. Adjusted net income attributable to Ryerson Holding Corporation, excluding restructuring and other charges, and loss on retirement of debt was $47.1 million for the first six months of 2019, or $1.24 per diluted share. Adjusted EBITDA, excluding LIFO was $113.7 million in the first six months of 2019 compared to $168.8 million in the first six months of 2018. Reconciliations of Adjusted EBITDA, excluding LIFO and adjusted net income to net income attributable to Ryerson Holding Corporation is included below in this news release.

Central Steel & Wire Results

As of June 30th, 2019, CS&W completed its first full year since Ryerson acquired it on July 2, 2018. Overall, CS&W exceeded expectations, albeit with stronger returns in the second half of 2018 compared to the first half of 2019. Ryerson continues to view CS&W as a company with strong commercial goodwill, but is working through operating challenges presented by CRU hot-rolled coil price deflation in the second quarter of 2019, while the base business remains consistent with our expectation of the operating model improvements necessary when we purchased the Company. CS&W was acquired with significant working capital which management continues to reduce to operate in-line with the Company’s same-store service center metrics. During the current deflationary cycle which began in August 2018 and continued through June 2019, CS&W experienced outsized inventory holding losses compared to Ryerson’s base business, with losses accelerating in the second quarter of 2019 given the significant decline in CRU hot-rolled coil prices during the period. CS&W incurred negative Adjusted EBITDA, excluding LIFO of $2.0 million in the second quarter of 2019 compared to our expectation of positive Adjusted EBITDA, excluding LIFO of $6.0 million for the period, and compared to $3.4 million in the first quarter of 2019. We expect inventory holding losses to dissipate in the third quarter of 2019 as hot-rolled coil prices appear to have stabilized, and CS&W’s inventory position has been reduced from almost 140 days at the time of acquisition to 91 days as of June 30, 2019.

Over the past year, CS&W surpassed nearly every post-close optimization goal by retaining nearly all customer accounts, achieving approximately $30 million of expense savings on an annualized basis from supply chain synergies and operational expense take-outs, and realizing $12 million of cumulative proceeds from real estate sales for operations that were consolidated into existing facilities. Management continues to believe in the long-term, mid-cycle target for CS&W of $600 million in revenue and $50 million in Adjusted EBITDA, excluding LIFO on an annual basis.

Liquidity & Debt Management

In the second quarter of 2019, Ryerson’s inventory balance stood at 75.3 days of supply, or 73.0 days on a same-store basis, up from 70.5 days in the second quarter of 2018. Our same-store inventory levels were within our target range of 70 to 75 days, while CS&W continued its commendable progress in moving inventory levels meaningfully closer to acquisition post-closing targets.

Cash generated by operating activities was $66.5 million for the second quarter of 2019 compared to cash used in operating activities of $49.6 million in the year-ago period, primarily driven by lower working capital requirements. We utilized our free cash flow to reduce our debt by $40.8 million and invest in capital expenditures of $12.1 million during the period. Ryerson expects to generate significant cash from operating activities in the second half of 2019 given lower replacement inventory costs in the third quarter of 2019, and seasonal inventory destocking expected in the fourth quarter of 2019. Ryerson maintained ample liquidity of $450 million as of June 30, 2019 to service our business.

Chief Financial Officer Erich Schnaufer said, “Ryerson remains committed to dedicating free cash flow to reducing our debt and lowering fixed cash commitments to meaningfully shift our enterprise value from debt to equity. Ryerson’s book value of equity continues to increase from $76 million as of December 31, 2018 to $131 million as of June 30, 2019, illustrating the continued strengthening of our balance sheet.”

Outlook Commentary

For the third quarter of 2019, Ryerson anticipates revenues of $1.075 billion to $1.125 billion with tons shipped down 3 to 5 percent compared to the second quarter of 2019 due to normal seasonality patterns and slowing end-market demand. Ryerson anticipates more significant volume declines in the oil and gas sector to be offset by relative strength in commercial ground transportation and construction sectors. Commodity prices are expected to stabilize and move modestly higher for carbon and stainless products, while aluminum prices are expected to be modestly lower for the remainder of the year. However, due to the lagging effects of replacement cost decreases experienced in the second quarter of 2019, as well as lagging contract formula pricing, Ryerson expects average selling prices in the third quarter to be down 3 to 5 percent. LIFO income in the third quarter is expected to be in the range of $26 to $30 million on accelerating movement of average inventory costs to replacement costs.

Ryerson anticipates margins to expand in the third quarter of 2019, and therefore expects earnings per diluted share in the range of $0.66 to $0.77 and Adjusted EBITDA, excluding LIFO in the range of $46 to $50 million. A reconciliation of Adjusted EBITDA, excluding LIFO to earnings per diluted share is included below in this news release. Ryerson expects to continue to deleverage given the continuation of counter-cyclical cash flows, meaningfully reducing long-term debt for the balance of the year.

Same-store Key Financial Metrics Reconciliation

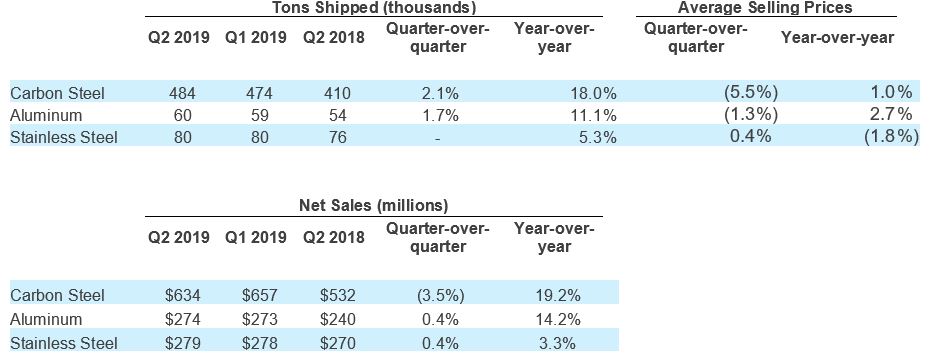

Second Quarter 2019 Major Product Metrics

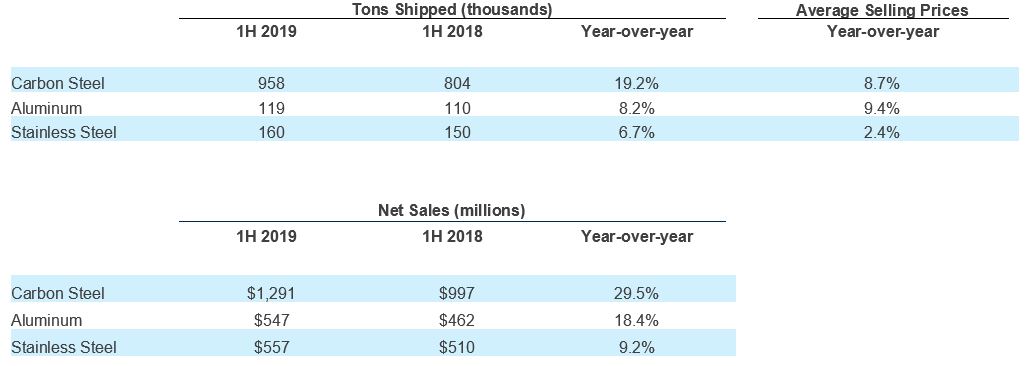

First Half 2019 Major Product Metrics

Ryerson will host a conference call to discuss its second quarter 2019 results Tuesday, August 6, 2019 at 10 a.m. Eastern Time. Participants may access the conference call by dialing 833-241-7253 (Domestic) or 647-689-4217 (International) and using conference ID 7623059. The live online broadcast will be available on the Company’s investor relations website, ir.ryerson.com. A replay will be available at the same website for 90 days.

About Ryerson

Ryerson is a leading value-added processor and distributor of industrial metals, with operations in the United States, Canada, Mexico, and China. Founded in 1842, Ryerson has around 4,600 employees in approximately 100 locations. Visit Ryerson at www.ryerson.com.

Safe Harbor Provision

Certain statements made in this press release and other written or oral statements made by or on behalf of the Company constitute “forward-looking statements” within the meaning of the federal securities laws, including statements regarding our future performance, as well as management’s expectations, beliefs, intentions, plans, estimates, or projections relating to the future. Such statements can be identified by the use of forward-looking terminology such as “objectives,” “goals,” “preliminary,” “range,” “believes,” “expects,” “may,” “estimates,” “will,” “should,” “plans,” or “anticipates,” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy. The Company cautions that any such forward-looking statements are not guarantees of future performance and may involve significant risks and uncertainties, and that actual results may vary materially from those in the forward-looking statements as a result of various factors. Among the factors that significantly impact the metals distribution industry and our business are: the cyclicality of our business; the highly competitive, volatile, and fragmented market in which we operate; fluctuating metal prices; our substantial indebtedness and the covenants in instruments governing such indebtedness; the integration of acquired operations; regulatory and other operational risks associated with our operations located inside and outside of the United States; work stoppages; obligations under certain employee retirement benefit plans; the ownership of a majority of our equity securities by a single investor group; currency fluctuations; and consolidation in the metals producer industry. Forward-looking statements should, therefore, be considered in light of various factors, including those set forth above and those set forth under “Risk Factors” in our annual report on Form 10-K for the year ended December 31, 2018, and in our other filings with the Securities and Exchange Commission. Moreover, we caution against placing undue reliance on these statements, which speak only as of the date they were made. The Company does not undertake any obligation to publicly update or revise any forward-looking statements to reflect future events or circumstances, new information or otherwise.

For full release details see ir.ryerson.com.